IV/Underlying Correlation

Devising an accurate options model can be tricky, particularly when IV is actually dependent upon price movements. This phenomenon is well known, and measurable in the Volatility Index (VIX) (it's ocasionally called the "fear index" by CNBC) for the S&P 500.

In general, large down moves in the S&P 500 will be met with correspondingly large up moves in the IV of options. At an extreme, during the stock market crash in 1987, the price of calls actually went up despite a 20% drop in the S&P.

Black (the offshoot of Black-Scholes designed for futures) assumes volatility as an independent input. With dependent volatility, delta-neutralizing portfolios becomes a challenge! Assume a delta neutral ES position. A 10 point drop in the underlying may result in a $2 loss, whereas a 10 point rise in the underlying may result in a $1 gain, solely because of the IV change. Obviously, a "delta-neutral" portfolio of ES options must actually be substantially delta-negative using the Black model.

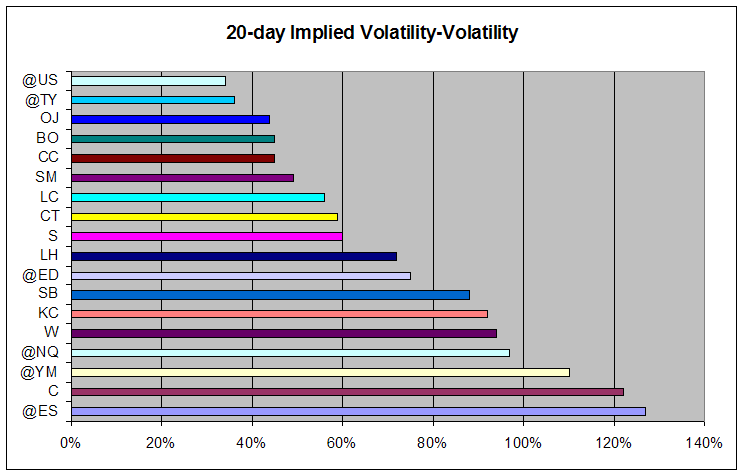

A look at the correlation of the underlying to its IV is helpful:

A correlation of 1.0 means the IV moves proportionally to the underlying. A correlation of -1.0 means the IV moves inversely proportionally to the underlying. The closer the correlation is to 1 or -1, the more predictable the movement of IV compared to the underlying.

A correlation of 1.0 means the IV moves proportionally to the underlying. A correlation of -1.0 means the IV moves inversely proportionally to the underlying. The closer the correlation is to 1 or -1, the more predictable the movement of IV compared to the underlying.As you can see, Russell (ER), Dow (YM), and S&P (ES) all have statistically significant IV movements opposite the underlying. (i.e. a rally will cause IV to drop). On the other side, Coffee (KC), Wheat (W), and Corn (C) have statistically significant IV movements along with the underlying (a rally will cause IV to rise).

In short, the index components need substantially delta-negative portfolios to be properly hedged while coffee and the two grains need substantially delta-positive portfolios.

These relationships are dynamic. Corn, for example, may have a correlation near 1 out of fear that a bad crop will cause substantial price increases, but a good crop will probably not cause too much of a price drop. During periods with limited reserves and high corn prices, the correlation would likely be the opposite. Presumably, if surprise Fed interest rate drops were more common than stock market crashes, the ES correlation would flip as well.

The ideal would be to modify Black to take into account these correlations to result in a truly hedged portfolio. If this work has been done, please tell us about it!

posted by FullyArticulate @ 5:48 PM

0 comments

![]()