IV volatility

While on the subject of second derivatives, ever thought about the volatility of IV?

43% IV on Coffee on 7/5 is near a very long term high. If you had purchased an ATM straddle on 7/5, and held it to 7/21, you would have lost .95 despite a rapid 8% drop in Coffee's prices. On the other hand, if IV had stayed a constant, you would have made .25 in the same time period.

43% IV on Coffee on 7/5 is near a very long term high. If you had purchased an ATM straddle on 7/5, and held it to 7/21, you would have lost .95 despite a rapid 8% drop in Coffee's prices. On the other hand, if IV had stayed a constant, you would have made .25 in the same time period.There are a variety of pure Vega trades which can make money no matter what the underlying does. Identifying targets for these types of trades requires a peek at the Volatility of the IV (IVV, to make up a term). A very low IVV means you can almost ignore IV and play purely on price action. A very high IVV means you better pay close attention to IV and its historical range before enterting a trade.

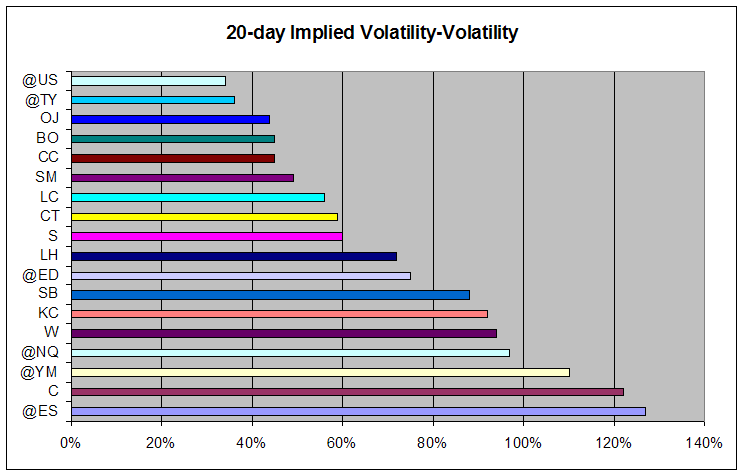

IVVs are pretty widely variable, but there are a few surprises. The S&P's IVV is substantially greater than the Nasdaq's, for example.

@ES having the highest IVV is particularly illuminating. In these days leading up to the fed meeting, IV is having far more impact on @ES option pricing than the small underlying price movements.

@ES having the highest IVV is particularly illuminating. In these days leading up to the fed meeting, IV is having far more impact on @ES option pricing than the small underlying price movements.

posted by FullyArticulate @ 5:22 PM

0 comments

![]()

0 Comments:

Post a Comment

<< Home